In this article:

This article explains how your balances can become "out of balance" and provides solutions for fixing the issue.

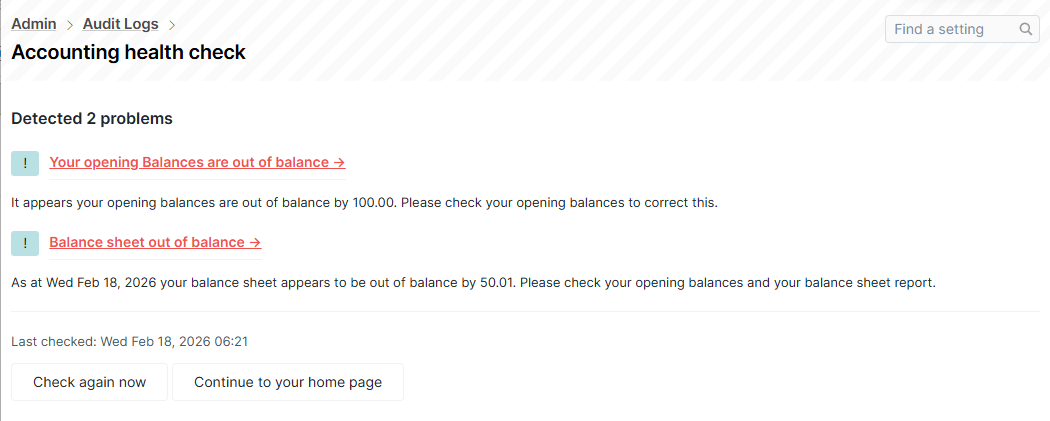

Reviewing Account Health Check Issues

Each day, Actionstep performs an automated health check on your system. If issues that are considered outside "normal" accounting practice are detected, admin users with access to Accounting will be alerted when they sign in to Actionstep. (Users without this level of access will not be notified.)

These notifications are displayed on the Health Check page (go to Admin > Audit Logs > Accounting health check). Once you have resolved the issues, you can use the Check again now button to make sure your changes fixed the issue. If you are not sure how to resolve the issues being reported, please contact your firm's accountant. To address the issues later, click Continue to your home page.

There are a few common problems that might create an out-of-balance error:

- Date of opening balances has been changed

- Opening balances are either incorrect or haven't been entered

- Multi-currency or foreign exchange settings are configured incorrectly

Issue 1: Date of Opening Balances Has Been Changed

In this scenario, make sure your opening balances date is correct. You can check this by going to Admin > Accounting > Accounting preferences and scrolling to the Financial dates section. Then make sure the date of the opening balance is correct.

Issue 2: Opening Balances are Either Incorrect or Haven't Been Entered

The opening balances and opening balance date that you have set up will have an impact on your balances. You can check this by going to Accounting > Accounts > Accounts List. If your accounts are out of balance, you will see an error like the following:

To review and edit the opening balances, click Edit Accounts. Then, review the information on the page and make any adjustments. If you're unsure of how to correct your opening balances, contact your accountant.

Issue 3: Multi-Currency or Foreign Exchange Settings are Configured Incorrectly

When using foreign exchange or multiple currencies, a number of accounts need to be set up. Additionally, some accounts should not be set up. (For help, see Configuring Multi-Currency/Foreign Exchange (FX) Billing (Admin) and Creating Multi-Currency Bills Using Foreign Exchange (FX) Billing.)

By mapping some accounts in multiple currencies, you can receive funds in multiple currencies and convert the value of that currency into the system's "base currency" before those balances are recorded in financial statements. This means that every balance shown on the financial statements (Income Statement, Balance Sheet, Trial Balance Report, Cash Flow Report) will display their balances in the base currency.

• Current Year Earnings and Retained Earnings are equity accounts seen on the balance sheet whose balance is calculated automatically by taking the sum of the Income statement (total income-total expenses). So basically, at any point prior to closing out a financial year, the total you see at the bottom of your income statement all flows into that one account on the balance sheet.

• Since all foreign currency conversion happens prior to any balances making it to the income statement, there is no reason to set up a separate Current Year Earnings and Retained Earnings account for each currency. So at no time should equity accounts be set up in a separate currency as it is not required and will cause an imbalance.

Additionally, if you updated your exchange rate on the date of the issue or entered an invoice with a different exchange rate and your system accounts are not correctly configured, it's possible that only one side of a transaction is correctly recorded.

To fix this, go to Admin > Accounting > System Accounts and make sure you have set up the following system accounts in the correct currencies:

|

|

Related Articles:

Was this article helpful?

That’s Great!

Thank you for your feedback

Sorry! We couldn't be helpful

Thank you for your feedback

Feedback sent

We appreciate your effort and will try to fix the article